Before applying for a loan in 2025—whether for a home, vehicle, business, or personal requirement—it is essential to understand the prevailing economic conditions in India. Macroeconomic indicators such as GDP growth, inflation, interest rates, and credit availability significantly influence borrowing costs and loan approval decisions. This article examines the key economic developments in 2025 and outlines their impact on prospective borrowers.

1. Economic Growth and Consumer Demand

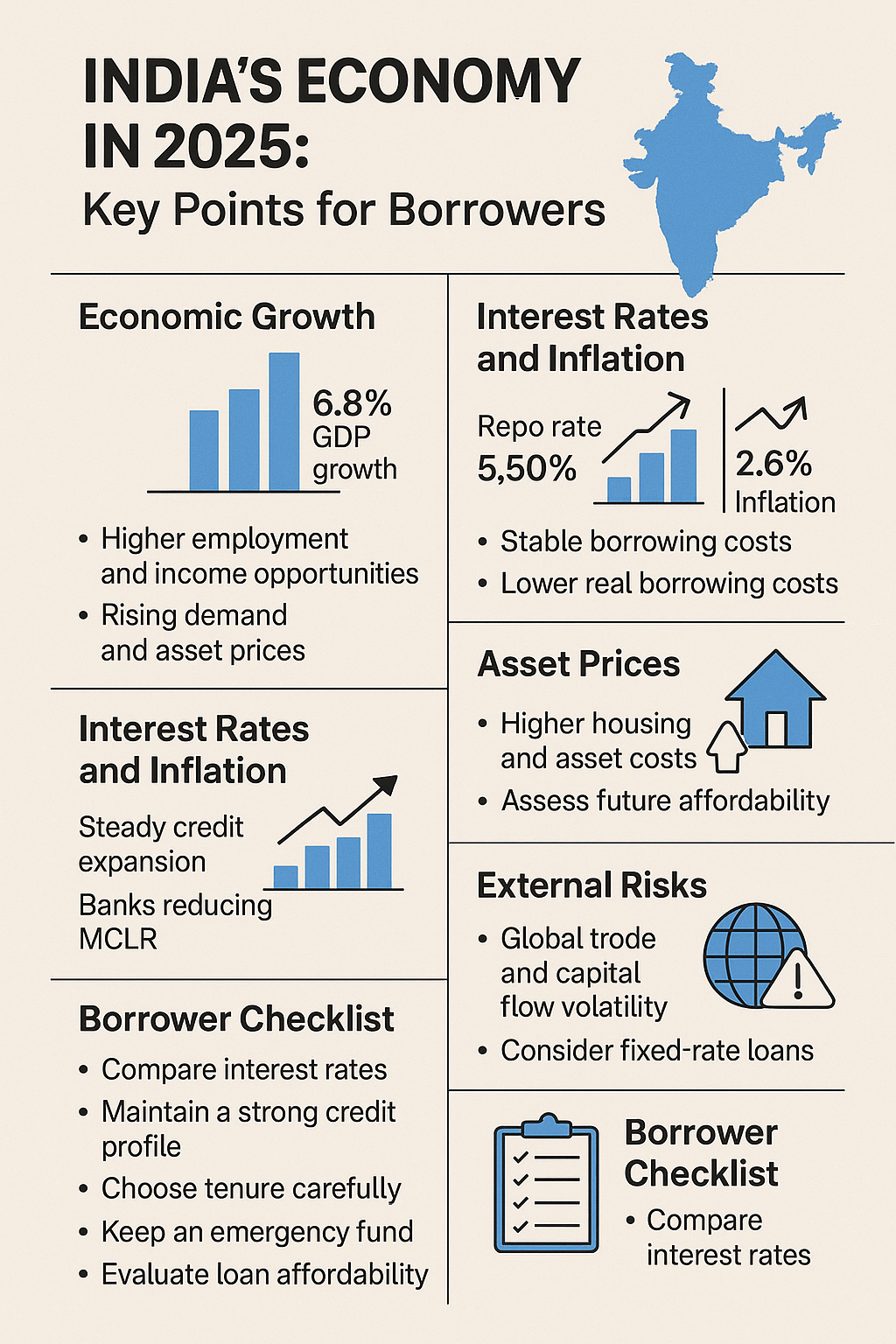

India continues to demonstrate strong economic resilience. For the fiscal year 2025–26, the Reserve Bank of India (RBI) has revised GDP growth projections to approximately 6.8%. The April–June quarter recorded 7.8% year-on-year growth, driven by robust private consumption and investment activity.

Implications for borrowers:

- Higher economic growth enhances employment opportunities and income stability, strengthening eligibility for loans.

- Increased demand for goods and services may cause rises in asset prices, prompting borrowers to opt for higher loan amounts.

- With expanding business activity, competition for credit may increase, making it important for borrowers to secure favourable lending terms.

2. Interest Rates and Inflation Trends

The RBI maintained the repo rate at 5.50% in its October 2025 meeting, indicating a neutral monetary stance. Meanwhile, inflation for FY 2025–26 is projected at a moderate 2.6%, supported by stable commodity prices and effective policy measures.

What this means for borrowers:

- Stable policy rates generally result in more predictable loan interest rates.

- Controlled inflation improves the real value of money and makes borrowing more cost-effective.

- Lenders may adopt stricter screening processes, prioritising applicants with strong creditworthiness and income stability.

3. Credit Growth and Lending Conditions

Credit growth has shown a steady upward trend. Bank credit expanded by nearly 10% in July 2025. Several banks have also reduced their Marginal Cost of Funds-based Lending Rate (MCLR) by 5–15 basis points to stimulate lending.

Borrowers should:

- Compare interest rates across lenders, especially considering MCLR, repo-linked lending rates, and associated margins.

- Maintain a strong credit score and low debt-to-income ratio to secure favourable loan terms.

- Focus on financial discipline, as lenders increasingly prioritise borrower stability over aggressive lending.

4. Housing and Asset Price Outlook

Rising demand and improving incomes have resulted in upward movement in real estate and other asset categories. While this is beneficial for long-term wealth creation, it also increases the cost of acquiring assets.

Borrower recommendations:

- Evaluate affordability using a conservative approach, factoring in possible increases in interest rates or temporary income fluctuations.

- Consider a higher down payment to reduce loan burden and secure better approval chances.

- Assess long-term financial commitments before finalising any high-value loan.

5. External Economic Risks

Despite strong domestic fundamentals, global risks such as geopolitical tensions, trade restrictions, and capital flow volatility continue to pose challenges. These factors may influence India’s borrowing costs, inflation levels, and overall economic stability.

Impact on borrowers:

- Lenders may tighten eligibility norms during global uncertainty, particularly for business or self-employed applicants.

- Borrowers must carefully evaluate the suitability of fixed versus floating interest rates depending on risk tolerance.

- Maintaining financial buffers is advisable to mitigate uncertainties such as rate fluctuations or income disruptions.

6. Borrower Checklist for 2025

Before applying for a loan, consider the following:

- Ensure your credit score is accurate and updated.

- Calculate your EMI after adding a stress buffer of 50–100 basis points to current rates.

- Keep your debt-to-income ratio below 40–45%.

- Select loan tenure carefully to balance EMI affordability with interest outgo.

- Compare multiple lenders and negotiate for lower margins and reduced processing fees.

- Maintain an emergency fund to avoid repayment challenges during uncertainties.

- Choose between fixed and floating rate options based on market expectations.

Conclusion

India’s economic environment in 2025 appears favourable for borrowers, with stable interest rates, moderate inflation, and robust growth indicators. However, macroeconomic stability alone does not guarantee advantageous loan terms. Borrowers must evaluate their financial readiness, credit profile, and long-term obligations before making borrowing decisions. A cautious and well-informed approach will ensure that loans taken in 2025 are sustainable and aligned with personal financial goals.